Berg Insight, the world’s leading IoT market research provider, today released new findings about the market for cellular routers and gateways.

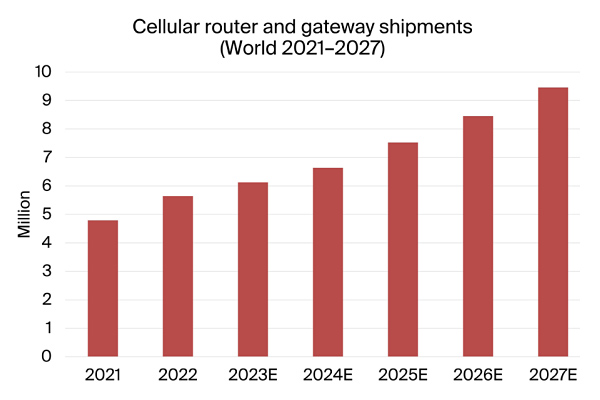

More than 5.6 million cellular routers and gateways were shipped globally during 2022, at a total market value of approximately US$ 1.4 billion. Annual sales grew at fast rate than shipments at a rate of 19 percent, reflecting strong customer demand in a constrained supply environment.

Several vendors reported that customers have built inventories during the last year to mitigate disruptions and delayed deliveries, which has resulted in a slowdown in sales growth in 2023. Even though long-term trends remain intact, cellular router vendors again face a more difficult operating environment in the short-term due to uncertain economic conditions. Until 2027, annual revenues from the sales of cellular routers and gateways are forecasted to grow at a compound annual growth rate (CAGR) of 12 percent to reach US$ 2.5 billion at the end of the forecast period.

Cellular routers and gateways provide primary or failover cellular connectivity to devices in a local network. The product category has evolved over the past decades from simple networking devices to aggregation points for devices, implementing advanced functionality for security and edge computing. The market is driven by the growing need to connect assets and workforces in remote and temporary locations as enterprises digitalise their operations.

Ericsson-owned Cradlepoint is the clear leader in the space and differentiates itself by selling its routers combined with software and services exclusively through a subscription model. Sierra Wireless, part of Semtech since early 2023, is the runner up and achieved strong sales growth during the year. Other vendors that hold significant market shares are Teltonika Networks, Cisco and Digi International. These five vendors generated US$ 808 million in combined annual revenues from the sales of cellular routers and gateways and hold a market share of 56 percent.

Other important vendors include BEC Technologies, Belden, Casa Systems, Lantronix, MultiTech and Systech in North America; Advantech, Four-Faith, Hongdian, InHand Networks, Peplink and Robustel in Asia-Pacific; and Eurotech, HMS Networks, RAD and Westermo in the EMEA region. The European and Asia Pacific markets are fragmented with a large number of small and medium sized players that generate annual revenues in the range of US$ 5–25 million.

5G routers and gateways now account for close to 10 percent of annual shipments, but a higher share of revenues due to the price premium to 4G LTE devices. While many distributed enterprises are already taking advantage of the fast deployment time and ease of use of cellular solutions, Berg Insight believes that the trend will accelerate in the 5G era. As the cost per GB decreases, 5G connectivity will become an increasingly attractive alternative to fixed broadband and over time reach a level in which the monthly fee is comparable to a fixed broadband subscription, thereby expanding the market for cellular routers, gateways and modems.