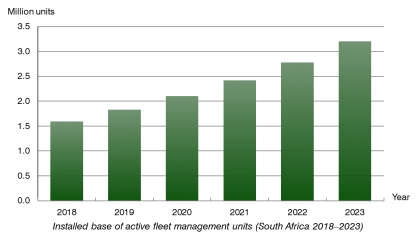

According to a new research report from the leading IoT analyst firm Berg Insight, the number of active fleet management systems deployed in commercial vehicle fleets in South Africa reached an estimated 1.6 million in Q4-2018.

Growing at a compound annual growth rate (CAGR) of 15.0 percent, this number is expected to reach 3.2 million by 2023.

South Africa is a relatively mature telematics market and the penetration rate is comparably high from an international perspective. Far from all deployments are however full-scale advanced FM solutions. A notable share of the installed fleet telematics systems on the South African market is represented by comparably low-end tracking systems, e.g. light FM solutions, including SVR systems extended with basic FM features.

“The South African fleet management market is clearly dominated by five domestic players with broad telematics portfolios, each having over 100,000 fleet management units in use in this market”, said Rickard Andersson, Principal Analyst, Berg Insight.

He adds that these top-5 players collectively account for more than two thirds of the total number of fleet management systems in use on the South African market.

“Berg Insight ranks Cartrack and MiX Telematics as the largest providers of fleet management solutions in South Africa, together having more than half a million active units in the country”, continued Mr. Andersson.

Tracker is the third largest player followed by Netstar and Ctrack (Inseego). Other top-10 players on the South African fleet management market include local providers such as Bidtrack (Bidvest Group), Digit Vehicle Tracking (Digicell) and GPS Tracking Solutions (Eqstra Fleet Management), as well as international players including Webfleet Solutions (Bridgestone) and Gurtam. Bidtrack’s owner Bidvest is notably in the process of acquiring Eqstra Fleet Management including GPS Tracking Solutions. Players just outside of the top list include Autotrak, Digital Matter, Pointer Telocation (PowerFleet), ACM Track, PFK Electronics, Geotab and Key Telematics.

“International commercial vehicle OEMs including Scania, Daimler, MAN and Volvo Group have further all introduced fleet telematics solutions in South Africa”, concluded Mr. Andersson.

Berg Insight’s report on Fleet Management in South Africa also includes an outlook on the overall African market. Africa is clearly a highly diverse geographic region from a fleet management perspective. The continent can in general be divided into three subregions – South Africa, Sub-Saharan Africa (excluding South Africa) and Northern Africa. The South African fleet telematics market is far ahead of the rest of the continent in terms of adoption, whereas Sub-Saharan Africa is the least developed region. Northern Africa is comparably advanced and well ahead of Sub-Saharan Africa when it comes to fleet telematics penetration, though still quite a bit behind South Africa.

Berg Insight’s report on Fleet Management in South Africa also includes an outlook on the overall African market. Africa is clearly a highly diverse geographic region from a fleet management perspective. The continent can in general be divided into three subregions – South Africa, Sub-Saharan Africa (excluding South Africa) and Northern Africa. The South African fleet telematics market is far ahead of the rest of the continent in terms of adoption, whereas Sub-Saharan Africa is the least developed region. Northern Africa is comparably advanced and well ahead of Sub-Saharan Africa when it comes to fleet telematics penetration, though still quite a bit behind South Africa.

The African fleet management market beyond South Africa is by many industry representatives described as challenging – though certainly also promising – for several reasons. The weak economic conditions and foreign exchange rate fluctuations in combination with the unstable political climate makes the Rest of Africa market a challenging business environment. There are however promising prospects for players adapting to the local market dynamics as the Rest of Africa market has considerably more untapped opportunity than what South Africa can offer at this stage.